Why the Atmanirbhar Scheme Is Not Really 10% of India’s GDP

Image for representational use only.

To contain the spread of the Novel Coronavirus, the central government closed the country’s borders and enforced a nationwide lockdown on 24 March, which has now been extended until 31 May. Despite all its efforts, COVID-19 infections and fatalities are growing every day. The country is thus under dual burdens: a public health catastrophe and an economic crisis.

When the Union Budget was announced in February it was expected that India’s economy would grow by 10% in financial year 2020-21. But as per estimates of the World Bank, India’s GDP growth may drop to between 1.5% and 2.8% during this fiscal year. Today the livelihood of millions of Indian workers is at stake. Around 40 crore workers, according to an ILO estimate, are at risk of falling deeper into poverty due this economic crisis.

There is no ambiguity among economists that India needs a fiscal stimulus to boost domestic demand and revive its economy. Additional government expenditure would have a multiplier effect on the economy. It would generate income and employment as well as encourage economic activities in the private sector, which can save the economy from a recession in the longer run.

That is why a lot of debate is being generated by the special economic package, the Atmanirbhar Bharat Abhiyan (ABA) worth Rs. 20 lakh crore announced by the central government on 12 May. Details of this package were unveiled in five tranches by the Finance Minister.

On the one hand is being argued that the comprehensive ABA would lay a strong foundation for raising India’s per-capita income. Some believe that it will increase the liquidity in the market and make the economy self-reliant. The counter-argument is that the package offered under ABA is far from the promised 10% of the GDP and that it inadequate to address the current economic crisis.

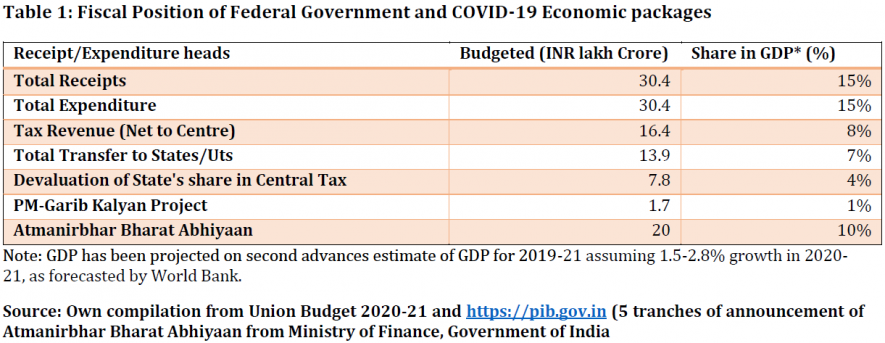

Table 1 describes the fiscal space in the latest Union Budget announced in February. The budgeted total receipts and expenditure were at Rs. 30.4 lakh crore (that is, 15% of the GDP) for the year 2020-21. Now, the central government has announced that the ABA would be 10% of the GDP. This means that ABA is the equivalent of 66% of the budgeted expenditure of the central government in FY 2020-21. Moreover, the proposed allocation for ABA exceed the central government’s tax revenues (recorded in the budget under the head “tax revenue net to Centre”).

Therefore, practically speaking, it is very difficult to accommodate the ABA into the available fiscal space in the 2020-21 budget.

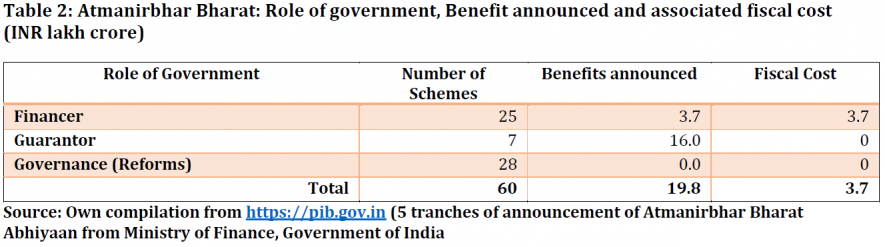

An even closer look at the schemes announced under ABA unveils the truth. Among the 60 broad schemes announced under it, the government is acting as the financer for 25 schemes. For seven schemes, the government is acting as guarantor, where loans or credit are to be provided by banks or other financial institutes. And 28 schemes announced under ABA are an array of measures and announcements that include redefining what is a micro, medium and small enterprise (MSME), revising labour codes, extending the income tax return filing deadline for FY 2019-20 and so on. (See Table 2).

It is in this way that the ABA has conceived of a benefit of Rs 19.8 lakh crore, while its fiscal cost would only be Rs. 3.7 lakh crore. This fiscal cost to the federal government includes additional government expenditures; for example the Rs. 40,000 crore hike in allocation for MGNREGS to boost employment, the Rs. 15,000 crore emergency health response package, the Rs. 7,500 crore support for EPF and so on. The fiscal cost also includes the revenue forgone, for example by the 25% reduction in rates of tax deducted at source and tax collected at source.

Expenditures that are already in the Union Budget 2020-21; for instance the devolution of taxes and revenue deficit grants to states and advance releases of the State Disaster Response Fund (SDRF) are not taken into account while estimating the fiscal cost of ABA.

It is also worth noting that the fiscal cost of schemes such as the “technology system” to be used to enable migrants to access the PDS (ration shops) anywhere in India by March 2021 was not announced. This scheme has come to be known as the “One Nation-One Ration Card” scheme. Nor was the fiscal cost announced for the scheme to provide “affordable rental housing” for migrant workers and the urban poor. This scheme is to be launched under a public-private partnership or PPP model. Furthermore, a majority of these schemes are not immediate interventions. Rather, they require a longer time horizon.

ABA was launched in five consecutive tranches. The fiscal cost of each tranche is detailed in Table 3. The third tranche of the announcement, which focuses on strengthening “agriculture infrastructure logistics, capacity building, governance and administrative reforms for agriculture, fisheries and food processing sectors”, has the highest fiscal cost (0.8% of GDP), followed by the first tranche, which focuses on “relief and credit support” to businesses, especially MSMEs (0.4% of GDP).

The tranche in which short-term and long-term measures for supporting the poor, including migrants, farmers, tiny businesses and street vendors was announced has the lowest fiscal cost so far. But the government did not disclose the details of two major schemes under this tranche either—that is, the “technology system” to enable One Nation-One PDS by March 2021 and the scheme for affordable rental accommodation, which is to be launched as a PPP.

There is a possibility that the government might spend more at the end of this financial year by bringing these schemes into operation. Even so, including all announcements in five tranches, the total additional fiscal cost for the federal government would be only Rs. 3.7 lakh crore—or around 1.8% of India’s GDP.

The ABA has taken some steps to provide cheap credit to farmers, medium and small-scale industries and businesses, but it does not look very promising to other vulnerable population groups such as the migrant workers and casual labours. Apart from the proposal to provide food grains, they are not entitled to any immediate relief.

Digitalisation of the mechanisms of the PDS is welcome, but immediate implementation of such a measure is not easy, especially when ration shops work with low-skill and low-wage labour. Credit and loans would improve the liquidity in the market, but it is not certain how much time it would take to infuse this liquidity, because economic activity has come to a halt due to the lockdown and the purchasing power of a majority of Indian families is adversely affected.

ABA will be successful in reviving the Indian economy only when it makes interventions that are tangible to the population and if it significantly improves the purchasing power of a majority of the population.

Pritam Datta is a fellow at the National Institute of Public Finance and policy (NIPFP), New Delhi and Chetana Chaudhuri is senior research associate, Public Health Foundation of India (PHFI), Gurugram. The views are personal.

Get the latest reports & analysis with people's perspective on Protests, movements & deep analytical videos, discussions of the current affairs in your Telegram app. Subscribe to NewsClick's Telegram channel & get Real-Time updates on stories, as they get published on our website.