India’s Industrial Sector: Myth and Reality

One of the elements of the so-called revival in GDP growth in the second quarter of the current year (2017-18) was an apparent rebound of manufacturing sector growth. The year-on-year growth rate of manufacturing, which had dipped to 1.2 per cent in Q1 of 2017-18 jumped to 7.0 per cent in Q2. On the face of it, therefore, the industrial sector is back on track after a brief demonetisation induced slowdown. That, however, may be no more than another instance of the completely misleading picture that the source of this data, the latest GDP Series with 2011-12 as the base year, tends to conjure of both the short- and the long-run state of India’s industrial sector.

Ever since the new GDP series came in 2015, the controversy around it has been particularly marked about the implications of the shift in the method used to determine the gross value added (GVA) in the manufacturing sector or its contribution to the country’s GDP. This shift involved measuring manufacturing gross value added, which is the difference between the gross value of output and the value of intermediate inputs consumed, at the enterprise level rather than at the producing establishment level as was the case earlier. One of the major reasons why there was a strong suspicion that this was leading to an exaggeration of manufacturing value added growth was the huge discrepancy between these growth rates emerging from the GVA data and those derived from the index of industrial production (IIP), which is a measure of output volume. While the former indicated robust manufacturing growth, the latter revealed a picture of complete stagnation from the second half of 2011-12. Both the GDP data as well as the IIP data, incidentally, are issued by the Central Statistical Organisation (CSO).

Recently, a new series of the IIP was introduced. Like the new GDP series, this too has 2011-12 as its base year (in the earlier series it was 2004-05). The stated objective of such revisions is “to capture structural changes in the economy and improve the quality and representativeness of the indices”. One would have thought that this new series would show an improved performance of the industrial sector compared to the older IIP series. While this did happen to an extent, its degree was not sufficient to eliminate the picture of industrial stagnation and eliminate the discrepancy between GVA and IIP trends of the manufacturing sector. This can be seen in Table 1 which shows the growth rates of manufacturing as measured by the three different indicators for each of the years after 2011-12.

Table 1: Rate of Growth of Manufacturing Sector by Alternative Indicators, 2012-13 to 2017-18 (H1) (Per cent per annum)

Table 1 clearly shows that while the manufacturing growth rate as per new series of the IIP never touched 5 per cent in any year between 2012-13 and 2016-17 and was below 4 per cent in three of them, as per the GDP series the growth rates over the same period never fell below 5 per cent per annum and in one year went close to 11 per cent!! What is additionally striking is that the acceleration in manufacturing growth from 2014-15 (when the current government took office) shown by the GDP data has no parallel in the IIP data. The difference between the two can be appreciated better by noting the following – the GDP series suggests that manufacturing output in 2016-17 was nearly 30 per cent more than in 2013-14, while the IIP data tells us it was barely 11 per cent greater.

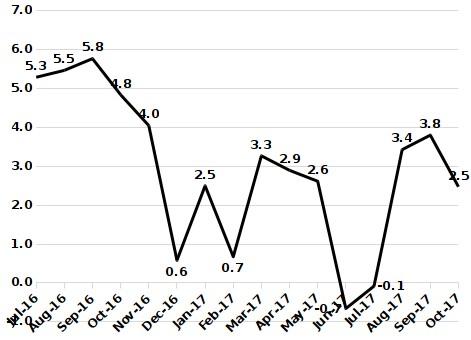

Exactly the same kind of variation can be seen in how the impact of demonetisation showed up in the two indicators of the state of manufacturing. As far as the GDP data are concerned, manufacturing growth appeared to have been severely affected only in Q1 of 2017-18 (several months after the withdrawal of legal tender status of the old 500 and 1000 rupee notes). The year-on-year manufacturing growth in Q3 of 2016-17, at 8.2 per cent, was even better than in the previous quarter and even in Q4 it was a reasonable 5.3 per cent. It has of course now revived to 7 per cent in Q2 after the dip in Q1. What the IIP data shows, on the other hand, is that demonetisation produced a fairly drastic adverse effect on industrial production even in relation to its already modest levels of growth, one from which it is still to recover. This is captured in Figure 1 which shows how the year-on-year growth of the monthly IIP moved between July 2016 and October 2017. The sharp dip from November 2016 onwards is clearly visible in this. The IIP data also shows that the improvement in Q2 of the current year over that of Q1 is far more muted than the GDP data indicate, and manufacturing growth remains depressed (and has dipped again in the first month of Q3).

Figure 1: Year-on-Year Growth of Manufacturing IIP (Base 2011-12), July 2016 to October 2017 (per cent)

The IIP trends shown in Figure 1 are clearly far more consistent with what should be reasonably expected to have been the effect of demonetization than the ups and downs of the manufacturing GVA growth over the same period. Indeed, the erratic behaviour of the latter defies any meaningful economic explanation and thus only serves to confirm its unreliability as an indicator of the state of Indian manufacturing. Thus, one can say that the manufacturing GVA growth emerging from the new GDP series on the one hand shows an acceleration that actually never happened - in manufacturing sector performance after the Modi regime came into being. At the same it hides the very real adverse impact of demonetization on that performance. Both ways it may have proved to be convenient for the Government’s propaganda purposes.

What is more serious, however, is that it is tending to create a veil over a longer-term process of de-industrialization being experienced by the Indian economy when everything else points toward it. Even in the new GDP series, the share of manufacturing in total GDP at current prices is declining consistently – and this should be set against a background where this share in the older GDP estimates had peaked way back in the mid-1990s. The levels of Investment in the manufacturing sector, through which production capacity is created and enlarged, has been stagnating for a decade – since the onset of the global crisis – and showing no signs of a revival. This, which is also keeping overall investment level in the economy depressed, is something that shows up again even in the new GDP series. Manufacturing employment growth has also been doing poorly – it had become almost entirely concentrated in organized manufacturing even before the current decade began and this too has started tapering off since 2011-12. India’s industrial sector is in a deep crisis – but those who want to assert the opposite are unlikely to do much about addressing its fundamental causes.

Get the latest reports & analysis with people's perspective on Protests, movements & deep analytical videos, discussions of the current affairs in your Telegram app. Subscribe to NewsClick's Telegram channel & get Real-Time updates on stories, as they get published on our website.