Putting Taxes to Work to Deter Smoking in India

Image Courtesy: Maxpixel

Taxing tobacco products is considered one of the most effective strategies among the six demand-reduction measures prescribed in the World Health Organisation’s Framework Convention on Tobacco Control. According to WHO, taxes must constitute at least 75% of the retail price of tobacco products. A Parliamentary Standing Committee Report published a few months before Union Budget 2023-24 reveals that in India, the prices of tobacco products are among the lowest and emphasises the need to raise taxes on them. In her budget speech this year, the Union Finance Minister proposed an upward revision of the National Calamity Contingent Duty or NCCD on cigarettes. However, there is no change for other tobacco products (bidi and smokeless tobacco products).

Taxes on Tobacco Products:

The Goods and Services Tax or GST, NCCD, central excise duty, and GST compensation cess are the four major taxes applicable on tobacco products. Central excise duties were initially subsumed during the initiation of GST. However, Union Budget 2019-20 reinstated this tax. A compensation cess was introduced for the first five years of the GST regime to compensate States for revenue losses. However, and importantly, no compensation cess was provided on bidi.

While GST is levied on all tobacco products at a 28% ad valorem rate (the tax amount is based on the transaction value), the NCCD and central excise duty are specific taxes where the amount of tax is fixed per unit of sale. The compensation cess is partly ad valorem and partly fixed (See Table 1). For example, the GST on 70 to 75 mm cigarettes is 28% of the retail price, whereas Rs 6.3 and Rs 5 per thousand sticks are levied as NCCD and excise duty. At the same time, 5% of the retail price over and above Rs 2,747 per thousand sticks is levied as a compensation cess on cigarettes with a length of 70 to 75 mm.

Proposed change in NCCD:

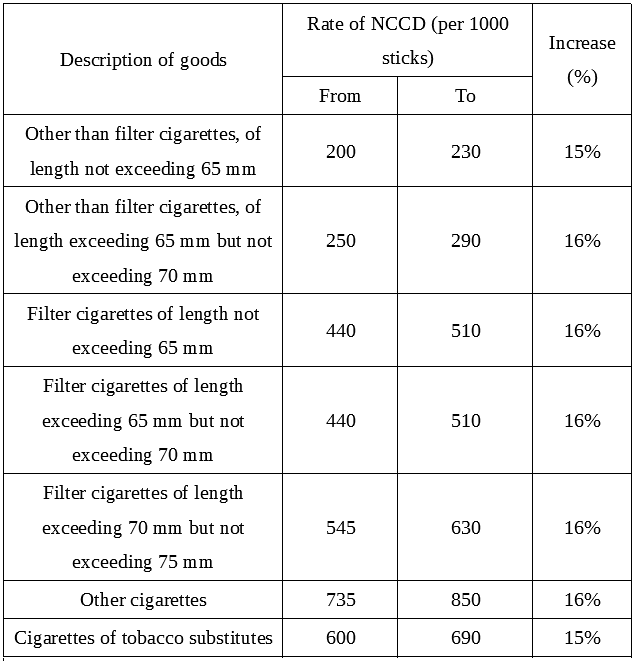

The Finance Minister only proposed changing the NCCD component on cigarettes in Budget 2023-24. It was increased by 15% for unfiltered cigarettes not exceeding 65 mm and 16% for unfiltered cigarettes between 65 and 70mm long. For all filtered cigarettes, the NCCD was raised by 16% (see Table 1).

A closer look suggests that the nominal increase of NCCD per pack of 10 sticks is only Rs 0.30 (30 paise) to Rs 1.16. The Global Adult Tobacco Survey India 2016-17 Report shows that 87% of cigarette smokers and 17% of bidi smokers bought loose cigarettes or bidis. And 25% of smokeless tobacco users bought loose smokeless tobacco products. Buying a single cigarette is common among the poor and the younger population who cannot afford entire packs or do not prefer to carry cigarette packs with them. Thus, to discourage smoking among this section of smokers, the tax per stick should be high enough to make even a single stick of cigarette unaffordable. It is important to remember there is not much of a revision in tax on tobacco products in the post-GST regime except for the reinstated excise duty in 2019–20 and the revision of NCCD on cigarettes in 2020-21 and 2023-24. A few-paisa increase in the per-pack tax on cigarettes cannot champion taxation on tobacco products.

Table 1: Changes in NCCD rates (in rupees) on Cigarette in Budget 2023-24

Source: Union Budgets 2020-21 and 2023-24

Bidi is the most common tobacco product among Indian smokers, consumed by roughly 72% of smokers. Often seen as a poor man’s luxury, it is kept outside the tax net. Other than 28% GST, an NCCD of Rs 1 per thousand sticks on hand-made and Rs 2 per thousand sticks of machine-made bidi—and excise duty of 5 paise per thousand sticks for hand-made and ten paise for machine-made bidi—is levied on bidi in India. A large part of bidi manufacturing is informal and thus manages to disguise itself from the tax or policy net. Cigarettes and bidis are a close substitute for each other. Tobacco consumption can be controlled with a differential tax rate increase for various tobacco products. All tobacco products need to be taxed with the common objective of discouraging tobacco consumption in the country.

Effect of minuscule but much-hyped increase in tax:

The gap between price inflation for tobacco products at the wholesale and retail levels is widening under the GST regime. The actual rise in cigarette price is a few paise only in nominal terms per pack cigarette. There has been no revision in GST rates on tobacco products in the last five years. However, minuscule modifications of specific taxes are hyped as big jumps in the tax burden.

Table 2: Gap between average increase in price of tobacco products at Wholesale and Retail level

Source: Author’s estimation based on wholesale and retail price index series.

This hype might work in favour of dishonest retailers who, with such announcements, start charging more for cigarettes, especially for loose sticks, even if the printed maximum retail price (MRP) does not change. The price hike on loose cigarettes over the rise in MRP goes into the pockets of tobacco retailers and would not reach tax authorities. As the transaction of loose cigarettes, bidi, and smokeless tobacco is more common in India, the retail price hike is greater than the hike at the wholesale level.

In other words, the higher price inflation of tobacco products at the retail level compared with the wholesale level shows that consumers are ready to absorb the effect of price hikes. That is why India must raise taxes on tobacco products much more than at present to make them unaffordable.

The author is a Fellow at the National Institute of Public Finance and Policy, New Delhi, and Honorary Fellow at the Foundation for MSME Clusters. New Delhi. His forthcoming piece will examine conditions in the bidi manufacturing sector. The views are personal.

Get the latest reports & analysis with people's perspective on Protests, movements & deep analytical videos, discussions of the current affairs in your Telegram app. Subscribe to NewsClick's Telegram channel & get Real-Time updates on stories, as they get published on our website.